Finding Your Limit and Why It Matters

Brad CollierPosted on April 1, 2022

Brad CollierPosted on April 1, 2022

Determining and selecting a building limit is one of the most important and challenging aspects of the insurance placement process. In the event of a covered property claim, the selected building limit will determine the amount of insurance funds available to an insured to repair/replace their damaged property.

Inadequate limits can lead to significant negative financial consequences for insureds, agents, and carriers. Despite the potential consequences, a study referenced in a 2017 Verisk article entitled “Ten Things a Commercial Property Underwriter Needs to Know1”, estimated that as many as 75% of all insured commercial buildings across the US are under insured.

Below we discuss some of the challenges that make determining replacement cost difficult, look at solutions available to insureds, agents, and carriers, and provide a brief explanation as to why adequate limits are so important to all three parties involved in the insurance placement process.

Determining Replacement Cost/Adequate Limit

Challenges

Lack of experience/expertise - Most building owners, insurance agents, and carrier underwriters do not possess the experience or required qualifications needed to accurately determine replacement cost. An agent who provides unqualified advice regarding the building limit can expose themselves to unwanted errors and omissions (E & O) claims.

Variability of construction quality, materials, design, etc. - Accounting for the many different variables that contribute to a building’s construction cost can be difficult. Differences in building height, footprint, types of build outs, facades, construction types, etc. can significantly impact repair/replacement costs.

Ambiguity regarding ownership of tenant improvements and betterments (TIBs) - Depending on the terms of the lease between a landlord and their tenant(s), an insured’s exposure may or may not include some/all of the TIBs inside the building (i.e. office buildouts, permanent restaurant equipment, cold storage equipment, etc.). Furthermore, it is common that the landlord will inherit ownership/insurance responsibilities for TIBs as of the termination of the lease which means an insured’s exposure can change over time.

Variations in cost by location - The cost of labor and materials varies dependingThe cost of labor and materials varies depending on the location of the risk. One builder, for example, estimates that a project in NYC can cost more than twice what it might cost in a Midwestern town. Prices can even vary in the same state. Consider two identical, above average, joisted masonry, 5,000 square foot strip mall buildings built in 2021, one built in San Francisco and one in San Diego. 360 Valuations of each property result in a recommended replacement cost for the San Francisco property that is approximately 12.5% higher than recommended for the property located in San Diego.

Inflation - Inflation causes repair/replacement costs to increase over time. The result is that the limit, adequate for a particular property, is a moving target and is not static. If unadjusted for inflation, a selected limit can quickly become inadequate, especially when inflation rates are high.

Catastrophes and unexpected changes in supply/demand - Supply shortages coupled with increased demand for construction materials and labor due to catastrophes or other economic conditions can cause significant increases to repair/replacement costs. The 2021 Oregon fires, for example, resulted in significantly increased lumber costs (3x increase), leading to an overall 25-30% increase in reconstruction costs. Recent Covid-related supply chain issues have further restricted availability of construction materials, causing construction costs to increase.

Older/historic buildings - Older and historic buildings can be especially difficult to value due to era-specific materials, construction methods, and architectural design. Due to the uniqueness of these types of properties, repair/replacement costs can be much higher than those for similar, more modern properties. In many cases, specialized forms/coverage are needed to address these type of buildings.

Cost of insurance - The financial incentive to lower premiums by selecting lower limits can tempt insureds to underinsure their properties.

Solutions

Replacement cost estimators - Online building valuation estimators, such as those provided by 360 Value and Marshall & Swift, provide estimates based on a variety of inputs (i.e. quality of construction, construction materials, roof type, square feet, etc.).

Appraisals - Replacement/reconstruction/market value appraisals by professional appraisers can help insureds determine the limit that fits their needs. For older/historic buildings, appraisers who specialize in historic replacement cost appraisals are best suited to determine replacement cost.

Extended replacement cost endorsement - An endorsement that provides an insured with a limit above the ratable value can help ensure the insured has an adequate limit in the event of a loss. The increased limit can help protect against reconstruction/repair cost increases that may occur during the policy term.

Blanket coverage - An endorsement that provides an insured with a limit above the ratable value can help ensure the insured has an adequate limit in the event of a loss. The increased limit can help protect against reconstruction/repair cost increases that may occur during the policy term.

Inflation guard - This provides an automatic annual increase to the property values to help offset effects of inflation and rising costs of construction. When applied regularly, it is designed to keep pace with replacement cost as it increases due to inflation over time.

Agreed value endorsement - This endorsement can be added in order to waive the coinsurance clause. A signed statement of values from the insured is often required by the carrier.

Periodic review of values - The replacement cost value of a building is subject to fluctuation over time. Building values should be reviewed and updated no less than annually in order to confirm continued adequacy.

Agent/underwriter experience - Insureds should look to work with agent/carrier professionals who are familiar with commercial property and have a good understanding of their insurance needs. While not able to provide the insured with specific advice regarding limits, agents/carriers can identify resources that can help determine appropriate limits and help them select forms/endorsements which meet their insurance needs.

Why Limits Matter & What Can Be Done

Insureds

Adequate insurance limits ensure availability of sufficient insurance funds so that the insured may be made financially whole in the event of a covered claim. For a building owner, this means being able to repair/rebuild a property of like kind and quality capable of generating the same rental income. Failure to carry an adequate building limit may result in an insured bearing a larger portion of the loss than contemplated as part of their risk management strategy. Underinsurance may leave the insured financially responsible for the difference between the building limit and actual repair/replacement cost. This can result in having to take on the additional financial burden of a loan, or, potentially worse, being unable to rebuild with like kind and quality, which can negatively impact the revenue the property is capable of generating.

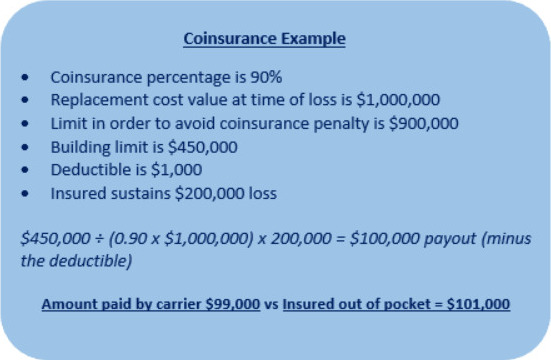

Furthermore, many policy forms include coinsurance clauses, which require the insured to carry limits equal to a stated percentage (i.e. 80%, 90%, 100%) of the replacement cost value at time of loss in order to avoid a coinsurance penalty. The limit required in order to avoid a coinsurance penalty is calculated by multiplying the replacement cost value of the property at time of loss by the stated coinsurance percentage. In the event the limit at time of loss fails to meet the stated coinsurance requirement, the insurance company will only pay an amount equal to the ratio between the building limit and the limit required to avoid coinsurance multiplied by the amount of loss, minus the deductible. Coinsurance penalties result in insureds having even less insurance funds available for repairs/replacement (note: coinsurance penalties can apply to both partial and total losses).

Regardless of whether it is due to the inadequacy of the limit or the imposition of a coinsurance penalty, the financial implications of underinsurance can jeopardize an insured’s financial viability and long-term solvency.

Agents

An agent’s reputation and viability are largely dependent on their ability to advise their clients properly regarding the insurance needed to address their exposures. Failure to place adequate insurance can result in dissatisfied clients and financially exposed insureds, potential harm to the agent’s brand/reputation, and/or claims against an agency’s E & O insurance. When it comes to limit selection, however, agents are forced to strike a balance between advising their clients without providing advice they are not qualified to give. Most agents, not qualified as building appraisers, may not want to recommend specific limits to their insureds. Instead, agents can advise their clients to select limits that avoid underinsurance or co-insurance penalties. To that end, agents might consider advising their clients to select limits that account for building characteristics such as:

- Actual square feet of the property, including mezzanines, common areas, etc. which may not be reflected on rent roll

- Location/accessibility of the risk

- Construction type/materials

- Building height/number of stories

- Type, amount, and quality of build outs

- Architectural design/features unique to their property

- Building footprint

- Roof type/material/design

- Age of the property and all updates

- Appurtenant structures and other property (i.e. fences, signed paved surfaces, etc.) at the insured premises which the insured wishes to cover

- Building systems (i.e. cold storage equipment, elevators, fire suppressions sprinkler system, alarms, etc.)

- Etc.

Additionally, agents can direct their insureds to available resources (i.e. reconstruction contractors, appraisers, etc.) which can help them determine an appropriate limit. They should also be prepared to explain the benefits/limitations of certain policy forms and endorsements and how they may affect the adequacy of the chosen limit.

Carriers

Property premiums are calculated by multiplying the selected rate by the ratable value of that property. For commercial buildings, the selected building limit is the ratable value. Inadequate limits negatively impact a carrier’s ability to achieve adequate premium for risk as loss costs exceed those contemplated by the premium charged. When a single risk is underinsured, the effect can be somewhat muted. When a large number of properties across a book of business are underinsured, it can jeopardize the viability of a program and the solvency of the carrier. Since carriers are not qualified replacement cost appraisers and often do not interact directly with insureds, carriers are not in a position to advise insureds regarding their limits. As such, defensive policy language, such as coinsurance clauses, are often included in their policies in order to mitigate effects of underinsurance and as a way to incentivize insureds to carry limits closer to the true replacement cost value of the building. Alternatively, carriers can charge an additional premium and have specific requirements in place in order to qualify for policies that include an agreed value endorsement.

Deans & Homer

How We Can Help

Determining replacement cost values for buildings can be challenging. A multi-faceted approach involving many of the solutions mentioned above can help decrease the potential for negative consequences associated with underinsurance for the insured, agent, and carrier. Deans & Homer’s unique approach to hands-on underwriting combined with proprietary, admitted commercial building products provide many of the tools to help agents and insureds avoid the negative consequences of underinsurance, including:

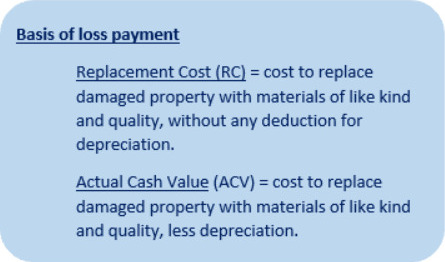

- Replacement cost basis of loss payment with no coinsurance clause included on commercial building policies.

- Extended replacement cost endorsement increases structure limit to 125% of the rateable value – available when the property is insured to value.

- Economic Replacement Cost (ERC) option – allows for coverage to be provided at an agreed value limit below replacement cost while still including a replacement cost basis of loss payment with no coinsurance clause (note: when this option is selected, the extended replacement endorsement is not provided and blanket coverage is not available).

- Blanket coverage available when insuring multiple properties (note: when this option is selected, the extended replacement endorsement is not provided).

- Broad definition of covered property which includes structures, signs, fences, light standards, paved surfaces, and appurtenant structures at the insured premises.

- Deans & Homer’s experience and specialization in commercial property means our underwriters are well prepared to discuss risks with agents to help ensure adequate coverage is in place.

Physical inspections of all commercial buildings allow underwriters greater insight into risk specific details that may affect a building’s replacement cost value.

Deans & Homer underwriters are ready to help agents and insureds face the challenges of determining adequate building limits and provide solutions that meet their needs.

- Peter De Freitas, “Ten Things a Commercial Property Underwriter Needs to Know”, Verisk, Sept. 26, 2017, https://www.verisk.com/insurance/visualize/ten-things-a-commercial-property-underwriter-needs-to-know/ (accessed Feb. 8, 2022).